When your company has grown significantly and reached a certain stage, it’s natural to consider your exit strategy. Today, there are more options available than ever before for private companies to tap into liquidity options, ranging from public markets to strategic outcomes.

Despite the uncertainty and economic turbulence of 2020, last year saw unprecedented activity across all fronts. According to Pitchbook and NVCA, there were 139 IPOs (the most since 2014), 250 SPACs—one of the main alternatives to traditional IPOs (with 5X growth year over year) and more than 700 US-based mergers or acquisitions (M&A).

As the numbers indicate, M&A present more liquidity options relative to the public markets. But acquisitions don’t just happen—there’s a lot that goes on behind the scenes and over time, that sets the stage for a successful M&A. I experienced this first-hand at Facebook, where I spent nine years in executive roles in corporate and business development. I led M&A efforts for the company, negotiated key partnerships, and served as a strategic advisor to product leadership teams across Facebook.

Now that I’m an investor, one of the questions I get asked most frequently is, “How do acquisitions come about?” In this post, I share my perspectives on this topic, starting with an abbreviated case study.

Behind the Scenes of the Facebook/Instagram Deal

In Spring 2012, Facebook acquired Instagram—just 18 months after the company’s launch. While the final deal was negotiated and inked over Easter weekend, Facebook CEO Mark Zuckerberg and Instagram founder Kevin Systrom had formed a relationship when Kevin was still in college at Stanford, and Mark was his mentor.

Over the years, the two entrepreneurs had developed a strong rapport and eventually were so aligned on a future together that the actual deal process was very short. Both wanted to serve the communities of people on their platform and create more ways for people to share. Instagram provided Facebook with a cool, new photo-sharing platform, and Facebook provided Instagram with a strong user base and resources to fuel growth.

Although this deal’s mutual benefits are still playing out, the numbers already tell a compelling story. Instagram had 30M monthly active users at the time of the acquisition. Today, the platform has over a billion monthly active users and has become a household name.

Build, Partner, or Buy

Large companies typically think about growth as stemming from one of three paths:

1) Build

2) Partner or

3) Buy

Let’s look at each one more closely.

When should you build?

A company will likely choose to build a new product or feature itself if it:

1) is a strategic asset or

2) includes some sensitive information or technology.

An excellent example of this is Facebook’s social graph, which represents people, places, and things, and the connections between them. These are the company’s crown jewels, and as guardians of this information, Facebook controls how this graph is built out and managed in-house.

When should you partner?

Alternatively, there is a strong case to partner when two companies’ goals line up in a mutually beneficial manner. For example, large companies might partner if they were standing up a new platform ecosystem or were looking to license technology to plug a product or service holes. The early days of Google’s Android ecosystem or Facebook’s licensing of HERE maps are good examples of this.

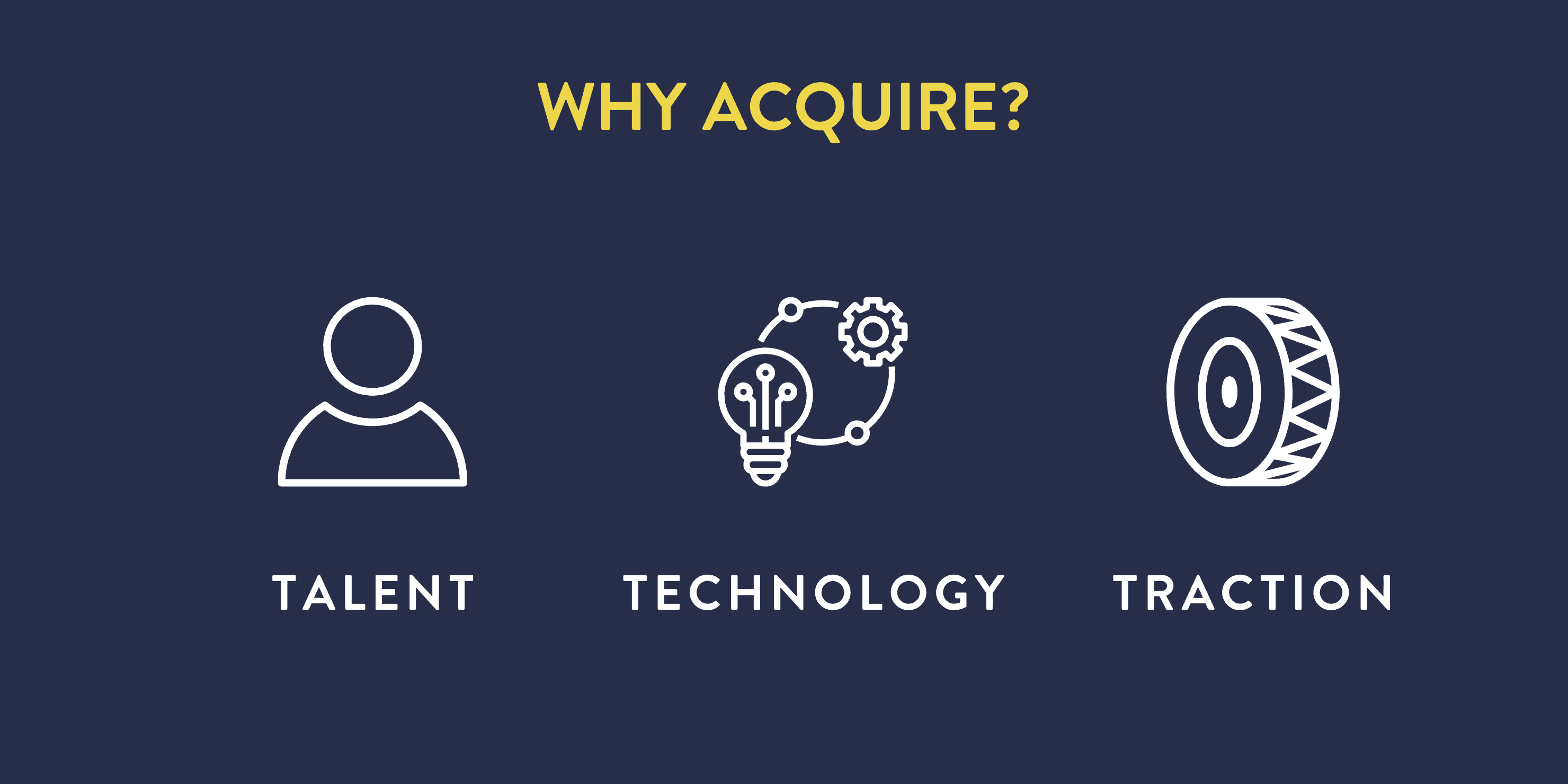

When should you buy?

Another path towards fueling growth is through acquisition or the “buy” scenario. Large companies will typically acquire for one of the following reasons—the 3 “Ts,” Talent, Technology, and Traction.

- Talent: Also known as acqui-hires, acquirers will buy smaller companies for teams in areas of hard-to-find talent, niche skills, or to fill a leadership gap. The founders’ pedigree and the team’s unique skill set are of most value in this scenario, typically resulting in massive retention bonuses for the team and minimal payout to the capitalization table (cap table) and investors.

- Technology: These are investments in a product or its underlying technology to jumpstart the acquiring company’s organic efforts. Amazon’s acquisition of self-driving technology company Zoox for $1.3B is an excellent example. In this scenario, the intellectual property around the technology would be of the most value, with free and clear patents in place. The payout is typically distributed between the team and the cap table, with significant variance on outcomes.

- Traction: This is when a large company buys into a new business by acquiring an established company. The WhatsApp acquisition by Facebook and the recent Slack acquisition by Salesforce are two examples. Metrics such as the number of monthly active users (and growth), revenue, number of customers, etc. weigh heavily on perceived value. Typically, the top players in the category command the greatest price.

What Makes an Acquisition Work?

Unfortunately, while a lot of acquisitions get done each year, few of them succeed. According to the Harvard Business Review, somewhere between 70 to 90 percent of all M&A deals fail. While investors and founders at target companies may be “made whole” with a financial exit, failure in this context means that an acquisition did not provide the intended value to the acquiring entity.

That said, Facebook has acquired more than 100 companies over its history, and I’d argue that most of these acquisitions have been successful. Similarly, companies such as Cisco and Google also represent the gold standard in M&A programs. So what is it about the way these companies approach acquisitions—and the companies they acquire—that have allowed them to beat the odds?

One thing it isn’t is the deal terms. The deal terms themselves are the least significant predictor of success—which might be a surprising sentiment from a former corporate development executive. In the Instagram example above, it was clear that the leadership on both sides had a shared vision—this is the most critical thing to get right.

The Founder’s Dilemma: Should I Stay, or Should I Go?

Facebook famously turned down a $1B acquisition offer from Yahoo in July 2006 when it had about 9M active users and $30M in revenue. It turned out to be the right decision for the company. But can you imagine having that conversation with your investors and senior leadership, and bringing them around to that conclusion at the time?

There is no easy way for a founder to decide between raising additional funding to invest in the business or selling the company. It’s a path every founder has to walk on their own. There are many factors to consider in every situation, but here’s one approach:

When not to sell

If you have a huge addressable market, with a proven product-market fit, and a good shot at being number one in that market, you may not want to be acquired. It’s likely in your best interest to remain a stand-alone company.

In addition to this logical analysis, you also have to consider the emotional aspects of the decision–are you willing to trade your dream of building a stand-alone business for another dream as part of another larger organization? What are the implications for you and your employees? Your investors?

When selling makes sense

On the other hand, if it’s clear that the acquiring company’s resources will help you realize your vision and have a more significant impact, selling makes sense. This is what we saw with Instagram. In this situation, selling the company would allow the founder to focus on the things they most care about, such as improving the product or scaling the business while removing distractions such as fundraising and negotiating office space.

In addition to providing financial liquidity for you, your employees, and your investors, selling your company might be a good option if the risk of remaining an independent company is too high.

If you are unsure which path to follow, you can always partner with a potential acquirer.

How Do You Build an M&A-Ready Company?

The decision of whether or not to sell your company is an enviable choice to have. But how do you build a company that makes that option available to you?

Make business development a priority.

As an investor, I always encourage founders to think about how to actively engage in their own ecosystem by networking as much as possible. Many founders are under the impression that being in “stealth mode” adds to the intrigue around what they are building. That can be true, but it’s also dangerous to be on an island – if no one knows who you are, how are you going to stand out in a sea of target possibilities?

Identify who your ideal customer or acquirer would be and find a way to build relationships with the senior-most leaders at that organization. You should leverage your investors, advisors, and former colleagues to make warm introductions to the appropriate people across product and business development teams. Once you’ve established a connection, take the time to understand that organization’s business priorities. Assuming there is alignment in priorities, share periodic product/progress updates to keep the relationships warm. You can take this a step further with a potential suitor by going back to the partnership framework we discussed earlier.

For example, you could volunteer to be a Beta partner for a new product where the company is attempting to boost its efforts. Or run a test where you provide the technology or service to bolster their offering. This will not only allow you to get to know the other company better, but it will enable you to showcase your unique advantages. Finally, it’s a great gift to large companies to get honest feedback from the market, which is often elusive.

Take the corporate development meeting.

I often get asked by founders, “Someone from corporate development at [company] reached out—should I take the meeting?” The short answer is yes! Corporate development teams understand the strategic priorities at their companies and the holes they are looking to fill. They are often looking three to seven years out, and want to establish relationships with companies and founders early. Use these meetings as an opportunity to get connected to product teams and company leadership and have them get to know you. These relationships are a key component of a successful M&A deal down the road.

Always be prepared

The old Scouting motto “be prepared” couldn’t ring more true than in this context. Now that you have the context of how acquisition decisions are made and understand the keys to make them successful, here are a few final things to keep in mind.

- Know what is important to you. What is your vision for your company? What outcomes are important to you? What qualities are you looking for in an M&A partner?

- Get your house in order. Get on the same page as your co-founders and board and take care of the less sexy stuff. This includes organizing your incorporation and financing documents, financial plans, IP and open source contributions, employment, and commercial agreements, and possibly even re-examining your corporate structure, if necessary.

- Be patient. Selling your company is an emotional, time-consuming experience that will take you away from running your business, much like fundraising. Lean on your board for advice. That Instagram deal that seemingly happened over the course of a weekend was actually years in the making. Keep that in mind.

With the framework I’ve outlined here, you can feel confident in building a company that is ready to embrace the right M&A partner if and when the time comes. It’s often said that “great companies are bought, not sold” – remember that strong relationships are the cornerstone of this truth.

***

At Norwest, our Partners and Portfolio Success team work together to ensure our companies are prepared to consider what potential exit is right for them and when to pursue it. We help you think through optimal strategy and positioning so our founders are empowered to understand all their options and be ready for any exit, be it M&A or an IPO/SPAC.